Microlending has become a vital tool for financial inclusion and small business growth, particularly in underserved areas. By providing small loans to individuals and enterprises without access to traditional banking, it fills a crucial financing gap. The global microfinance market is rapidly expanding and is expected to reach nearly $377.1 billion by 2030, highlighting the growing demand for small-scale lending solutions worldwide.

A micro-lending franchise enables entrepreneurs to operate under an established brand, offering loans while benefiting from a proven business model. With low startup costs and strong social impact, micro-lending franchises are increasingly popular among those seeking profitable ventures that empower communities.

This blog will explore what micro-lending franchises are, their importance, challenges and benefits, and how to get started in this growing sector. Whether you are a new entrepreneur or expanding in financial services, micro-lending franchises present an exciting opportunity.

A micro-lending franchise is a type of business arrangement in which entrepreneurs, referred to as franchisees, offer small loans to people or small enterprises while using the name and organisational framework of a more well-known, bigger franchisor. This enables franchisees to provide financial services to communities that are underserved, particularly in places where conventional banks and financial institutions have limited access.

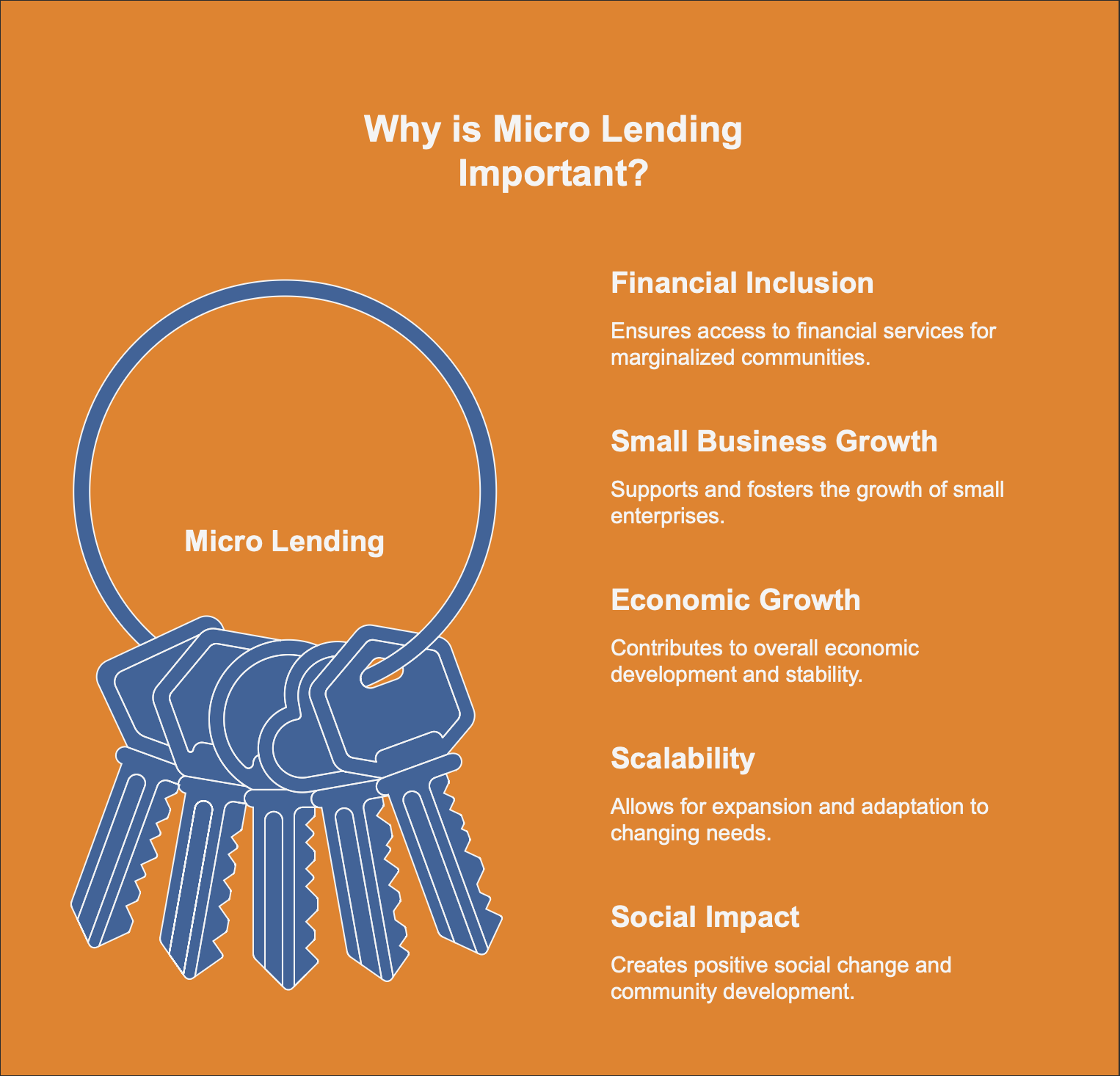

With the fundamentals of a micro-lending franchise addressed, let's look at why micro-lending is so essential and how it promotes monetary inclusion and economic development.

Micro financing is vital to small firms and people who cannot access standard banking services. Many people, particularly in developing countries, lack credit or savings options. Micro financing fills this vacuum, promoting economic development and social mobility.

One of the main advantages of micro-lending is its part in advancing financial inclusion. Micro-lenders enable people to raise their standard of life by providing modest loans to companies and individuals unable to qualify for conventional bank loans. Access to micro-credit may greatly improve financial security and opportunity whether one is using it for personal needs, launching a small company, or funding education.

Micro-lending helps sustain small enterprises, particularly low-income ones. Small loans enable business owners to buy supplies, inventory, or tools to grow their businesses. Often the foundation of local economies, these companies may flourish and provide employment with the support of modest, reasonably priced loans. For small business owners, having financial access may be a game-changer as it enables them to expand and enter a rising market.

Micro-lending enables individuals and firms to have the financial means they need, therefore promoting economic development. Spending rises, local economies boost, and employment prospects grow when more individuals and companies have credit access. Micro-lending not only helps the receivers but also advances the general economic growth of nations and communities.

Scalability provided by micro-lending franchises lets business owners expand into new areas or increase loan amounts, thereby strengthening their operations. Micro-lending companies frequently operate with adaptable, low-overhead models, and therefore franchisees may rapidly increase their client base or add additional loan agents. Entrepreneurs wanting to expand their company over time find this scalability appealing as a business strategy.

Apart from the financial benefits, operating a micro-lending franchise has among its most satisfying features the social effect it generates. Giving credit helps people to better their lives—for establishing a small company, funding education, or paying for basic needs among other things. Encouragement of economic mobility and enhancement of underprivileged communities' quality of life depend mostly on franchisees.

Microlending has a significant impact on small businesses, financial inclusion, and economic development, making it a valuable tool for addressing financial inequality. Let’s look at some of the challenges that franchisees may experience in the microlending market.

Also Read: Developing a Food Franchise Business Plan: Steps and Structure

Despite its enormous potential, the microlending franchise model has a unique set of challenges that business owners must take into account. Knowing these difficulties will enable franchisees to more successfully plan and negotiate the complexity of this business model. Micro-lending franchisees often deal with these typical challenges:

The microlending business is strictly regulated in most countries, including India. Local financial rules must be followed by franchisees including loan restrictions, interest rate limitations, and reporting requirements. Following these guidelines may be difficult, particularly in areas where complicated or often changing financial restrictions apply. To prevent fines or legal problems, entrepreneurs must keep updated on the legal environment and make sure their activities satisfy all regulatory criteria.

Giving loans usually carries some risk. Micro-lending, by definition, is lending to people or small enterprises with poor credit histories or uncertain financial situations. Loan defaults carry more risk than in more conventional lending systems. To reduce defaults and guarantee financial stability, franchisees have to use efficient risk management techniques like credit scoring, debt collecting procedures, and comprehensive borrower evaluations.

The microlending market has attracted a wide range of businesses, including conventional financial institutions and internet lending platforms. Franchisees have to set out their services differently to distinguish out given growing competition. This might imply providing speedier approval times, specific lending products, or better customer service. Maintaining competitiveness in this fast-expanding sector depends on keeping up with consumer expectations and market developments.

Growing new customers for a micro-lending company calls for strong outreach and marketing plans. Since micro-lending typically helps people who may be inexperienced with financial institutions or have debt worries, franchisees must develop trust within their communities. Upholding client loyalty and recurring business depend mostly on developing long-term connections and offering first-rate customer service.

Even while micro-lending franchisees usually have less overhead than conventional businesses, controlling running expenses may still be difficult. Franchisees must make sure they can quickly handle a lot of loans. Maintaining cash flow also depends on guaranteed regular repayments and efficient loan recovery. Franchisees must have explicit debt monitoring and recovery systems as well as clear regulations.

Micro-lending franchises can succeed and provide notable returns even with these obstacles if they have the correct plans and assistance. Understanding these risks and making appropriate plans would help entrepreneurs to manage a profitable micro-lending company by reducing their obstacles.

Micro-lending franchises provide a unique opportunity to create a successful business and improve your neighbourhood at the same time. Here are the reasons this approach is growingly appealing to entrepreneurs:

Micro-lending franchisees have significant earning potential as loan interest is the main source of income. For franchisees, microloans' interest rates and periods for repayment provide a consistent income flow. The earning potential rises as the franchise expands and more loans are distributed. Particularly when repayments for loans are collected effectively, this is a viable strategy because of the ability to grow micro-lending companies and reduced running expenses.

Micro-lending has great social influence beyond financial benefits. Franchisees enable communities by lending modest loans to both individuals and businesses that may otherwise have restricted access to credit, therefore promoting financial inclusion. By enabling small enterprises to flourish, this not only enhances borrower quality of living but also boosts local economic development. Many business owners find great inspiration in this mix of social good and profit to join the micro-lending sector.

Micro-lending programs often have quite minimal running expenses as compared to conventional businesses. Large physical stores or considerable inventory are not necessary, hence overheads are easy to handle. Often running smaller branches or even virtually, franchisees minimise the need for costly real estate. This frees up more attention for processing loans and customer service than for handling a significant infrastructure.

Access to financial services is usually restricted in developing nations, and demand for microloans is growing. Many people and small companies in these areas are looking more and more to micro-lending options as they lack access to conventional banking systems. Participating in this expanding market helps franchisees satisfy this increasing need and present one another for long-term success.

The micro-lending franchise model is easily scalable. Once the business model is established in one location, expanding to other regions or increasing the loan volume can lead to greater profitability. With the support of a franchisor, franchisees can replicate the model across different markets, benefiting from a streamlined process that ensures consistency and reduces risks.

Franchisees use the franchisor's brand and structure, but micro-lending gives entrepreneurs more freedom to run their businesses. Franchisees may customise their loan products to match their target market's demands while using the franchisor's established business model.

For entrepreneurs, micro-lending franchises provide a unique mix of profit, scalability, and social impact. This strategy has great benefits whether your goal is to create a financially successful company or help your community to flourish. Micro-lending franchises may be a profitable and significant endeavour with the correct training, tools, and support.

Also Read: Leading Benefits and Reasons for Owning a Food Franchise

Kouzina's franchising approach presents a great opportunity for business owners to join a low risk, highly sought-after sector with significant backing. Kouzina offers expandable cloud kitchen solutions that are essential in developing economies, thereby enabling food entrepreneurs to flourish, much like micro-lending franchisees give financial inclusion and assistance to small enterprises.

Kouzina's cloud kitchen concept is meant to let franchisees create lucrative food companies with low start-up capital and flexible scalability. Operating many food businesses under one roof, franchisees meet the increasing need for delivery-oriented food services. This method is ideal for Tier 2 and Tier 3 cities, where the demand for rapid, high-quality food delivery is rising yet restaurant setups are expensive and inefficient.

By leveraging Kouzina’s proven business model, franchisees receive:

Kouzina is easy to start and support, making it suitable for food investors. See how Kouzina partners describe working with them.

Kouzina's franchise model is altering the way food companies are managed, providing low-risk, high-reward prospects for entrepreneurs ready to take advantage of the growing food delivery sector, the same way micro-lending franchises are transforming access to financial services.

Micro-lending franchises offer a promising opportunity for entrepreneurs seeking to enter a growing and impactful sector. By providing small loans to underserved communities, you can build a successful business while promoting financial inclusion and local economic growth.

Though challenges like regulatory compliance and risk management exist, support from an experienced franchisor and a proven business model can help you navigate them effectively. If you’re motivated by both profit and positive community impact, a micro-lending franchise could be the right venture. With proper planning and partnership, you can establish and grow a rewarding micro-lending business.

Explore the best franchise management software and learn how Kouzina's cloud kitchen solutions can optimise your food business. Contact us now!

A micro-lending franchise is a business model where entrepreneurs provide small loans to individuals and small businesses under the guidance and branding of an established franchisor. This arrangement offers a proven framework, training, and ongoing support, enabling franchisees to operate efficiently while promoting financial inclusion.

Startup costs vary depending on the franchisor and location but are generally lower than those for traditional banking businesses. These costs usually cover licensing fees, training, marketing, and initial loan capital. The relatively modest investment makes this sector accessible to entrepreneurs entering financial services.

Micro-lending provides credit to people excluded from conventional banking, such as low-income individuals and small enterprises in underserved communities. Access to finance helps these groups grow their businesses, improve their livelihoods, and participate more fully in the economy.

The main risks include loan defaults and compliance with financial regulations. Effective risk management, thorough borrower assessment, and continuous support from the franchisor help mitigate these challenges and sustain business operations.

Begin by researching reputable franchisors and understanding their business models. Assess market demand in your target area, familiarise yourself with relevant legal requirements, and participate in the training and support programmes offered by the franchisor to build a strong foundation for your venture.